🐋 Whale’s Brief: 5 Costly Errors-and 3 Smart Escapes

Good day, dear reader — Whale Investor here.

The market’s next storm looms quietly on the horizon, a subtle shift in the tides that many seasoned investors sense but few openly acknowledge. For affluent Americans navigating the twilight years or preparing for that moment, the calm surface of conventional retirement planning masks a series of undercurrents that threaten hard-earned wealth. Most quietly rely on familiar tools like 401(k)s and IRAs — instruments often treated as safe harbors but slippery when inspected closely. While Wall Street chases momentum and speculation, those who study the deeper rules—the ones below the surface—know true security comes from strategic nuance. The question is not if but when and how to steer through peril and opportunity alike. The pathways to preservation and growth exist, yet well-hidden. This brief uncovers those currents.

Five Common Pitfalls in Retirement Wealth Management

Retirees and pre-retirees often drift unknowingly into costly mistakes that erode their longevity and independence. The first problem is excessive cash holdings. While it feels prudent to sit on cash during volatile times, inflation relentlessly devours purchasing power, turning conservatism into a slow leak. Cash here is no refuge; it is a current pulling capital downstream.

Secondly, many assume tax-deferred accounts are intrinsically safe, skillfully avoiding immediate tax bills. This surface-level appeal misses the broader picture: taxes are deferred, not eliminated. Withdrawals in retirement often trigger sizable tax hits tied to ordinary income rates, and recent policies threaten to raise these further. This is deferred vulnerability, a tide pulling unseen.

A third undercurrent is the blindness to currency risk amid de-dollarization pressures. Americans seldom factor in the potential risks tied to a weakening dollar or shifting global reserve currencies. Ignoring this risk erodes real wealth, much like unseen ocean acidification slowly weakening coral reef foundations.

Next is the reliance on Wall Street-managed funds where active management and fees quietly erode returns. Many surrender control to opaque layers of middlemen, sacrificing independence and agility. It is akin to entrusting one’s navigation to a slow ship buffered by corporate interests—not the best way to survive rough seas.

Lastly, and most overlooked, is the failure to leverage advanced IRS strategies and legal tax shields. Many investors miss opportunities coded into the tax law itself, leaving wealth exposed to unnecessary taxation and asset compression. These missed maneuvers mean the difference between being battered by waves or riding above them.

These challenges share a root problem: a lack of strategic awareness about the rules and the shifting financial seascape. Without precision and insight, wealth preservation becomes mere wishful thinking.

Three Strategies to Protect and Grow Wealth in Retirement

For those aware of these undercurrents, the course to true security requires decisive navigation through diversification, control, and advanced strategy.

Solution One: Unlock the Power of IRS Code 408(m)

Did you know there’s an IRS loophole—408(m)—that lets you pull monthly or weekly income from your 401(k), IRA, TSP or 403(b) completely tax-free?

Most Americans have never even heard of it. Yet the wealthy use it to shield gains, avoid penalties and stay fully invested—while everyone else sits exposed.

This isn't a theory. It’s a legal, IRS-approved strategy that can put a second, tax-free paycheck in your pocket—no cash conversion, no red tape, no catching penalties.

Grab your FREE 408(m) Guide now

Stay protected when the next crash hits.

P.S. Wall Street won’t tell you about 408(m). The insiders move first. Claim your guide (and bonus gold coin) before everyone else wakes up.

Solution Two: Diversify Deeply Across Asset Classes

The first safeguard against inflation and systemic shocks is robust diversification—not just across stocks and bonds but into real assets like gold, innovative sectors like artificial intelligence, commodities, and select digital assets. This broad exposure hedges against different types of risk tides—purchasing power erosion, geopolitical upheaval, and technological disruption. Owning gold, for instance, anchors portfolios amid fiat currency uncertainty and monetary inflation. Meanwhile, selective digital assets can capture growth from the evolving global economy.

Solution Three: Embrace Alternative Assets and Tax-Optimized Structures

Affluent investors should also explore alternative assets within self-directed IRAs and tangible asset reserves. These options move beyond the Wall Street maze and grant real autonomy over wealth storage. Such structures enable ownership of physical real estate, precious metals, and other non-traditional vehicles, providing a hedge against market manipulation while opening avenues for lawful tax optimization. The key is acting within IRS rules but taking control away from centralized influence.

🌊 Whale’s Fact Break

Blue whales can slow their heartbeat to just two beats per minute when diving—a reminder that in deep waters, survival belongs to those who stay calm and conserve strength until the perfect moment to rise. Likewise, in investing, patience and strategic depth often yield far greater rewards than frantic surface paddling.

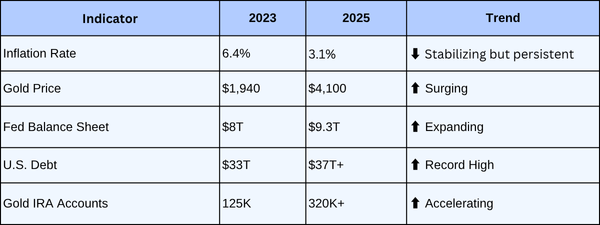

Data Snapshot 📊

Allegiance Gold

A legal, IRS-approved strategy that can put a second, tax-free paycheck in your pocket—no cash conversion, no red tape, no catching penalties.

🐋 Whale’s Final Word

True retirement wealth preservation isn’t about chasing fleeting yields or noisy market fads — it’s about reading the currents beneath the surface with clarity and calm. The tides of inflation, taxation, and geopolitical shifts require more than passive drift; they demand deliberate, informed action guided by insider knowledge and strategic diversification.

Move beyond common pitfalls with precision. Take control through lawful structures. And embrace proven yet little-known strategies like 408(m) that offer uncommon protection. The next wave will reward the prepared who swim steady through uncertainty.

Swim protected,

- Whale Investor 🐋